Apr 7, 2026

Sigma Lithium is a pure play high-quality lithium extraction in Brazil with a focus on ESG compliant extraction methods which makes it a preferred partnered for the coming western supply chain for one of the most critical energy hardware narrative of the next year: batteries.

Sigma Lithium Corp

Ticker: $SGML

Much more classic within a well-known sector, a small capitalization still at ~$1.6B but with “less” execution risks and clearer demand for its products as we are talking about lithium - as advertised in the name. Sigma is a pure play on high quality lithium extraction, operating in Brazil with a few twists, transforming it from just another lithium player to a potential great opportunity.

First, the company certifies a “quintuple green extraction” (zero coal power, zero tailings dams, zero utilization of potable water, zero use of hazardous chemicals and zero accidents), which you might not care about but many companies do as they have environmental restrictions – the famous ESG regulations. This became important as most of the resource comes from China or Chinese operated mines and doesn’t answer these regulations.

As the west is working on independence from extraction to refining and focuses on ESG-approved commodities, Sigma will receive more demand - as my second point will confirm.

Second, the company signed a $100M collateralized bank guarantee fully collateralized by its own clients through a blend of corporate guarantees, letters of credit and export receivables to be mutually agreed. This is the equivalent of Meta and Microsoft pre-paying for Nebius’ compute before it is installed, highlighting the demand for its products and allowing them to invest healthily in their second Greentech plant to double production from 270,000t to 520,000t annually.

Healthy balance sheet and the financing to double their capacity – hence revenues, in the medium term. This comes with execution risks obviously but this is excellent news for the financial health of the company and its growth profile.

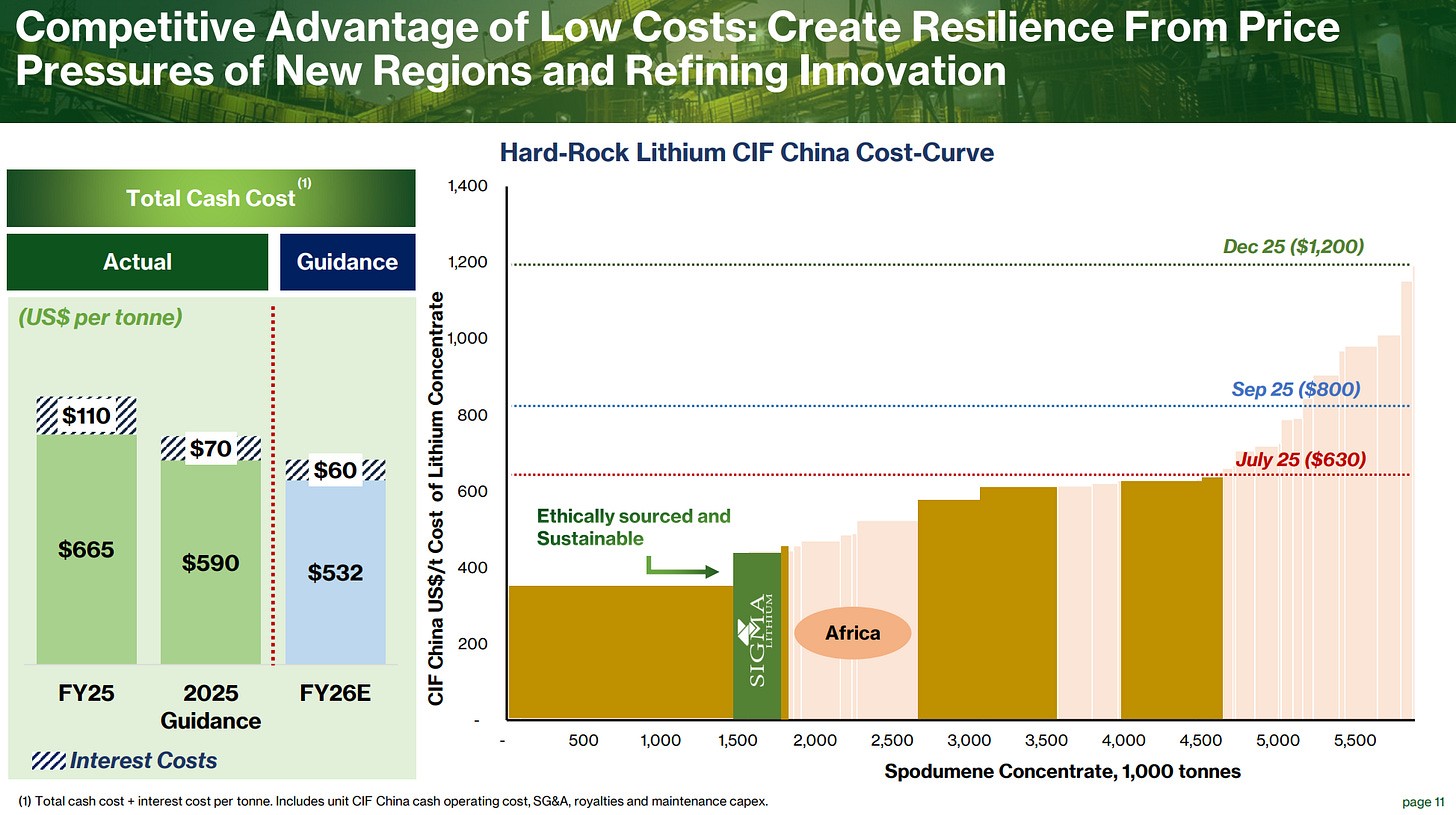

Third, as a pure play lithium extractor, Sigma is optimized with ~40% operating cash margins – pretty high for a commodity miner, and extracts the commodity for cheaper than competition - hence very competitive on the market.

Sigma is guiding to a $592/t extraction and shipping of their lithium, which puts them on the lowest extraction price on the sector - green position on the chart, while the red, blue and green lines are their profitability margins depending on lithium’s price, which as we’ll see has been rising and sits ~$2,000/t today.

Fourth, the geopolitical situation helps western companies with Trump’s tariffs forcing local production - Brazil isn’t local but it is close from U.S. factories which are being built to refine the raw material locally, while battery productions are already within the U.S. for some companies. As the continent works on building a supply chain locally - meaning without China, Sigma will become a logical go-to partner.

Natural resources are also on the rise for many reason - geopolitics and fears of supply chain shocks, raising oil being, refocus of liquidity… Raising resources are never great for an economy but we can benefit from it.

Lastly, the dollar falling is a big tailwind for Latin America comapnies as most of their loans – as confirmed with Sigma’s own loan, are denominated in dollars while their expenses to pay local workers and resources are in local currencies. I’ve wrote about this currency mix and how it impacts LATAM on MercadoLibre’s thesis.

In summary, Sigma is an optimized pure play with a very healthy balance sheet, an accelerating growth profile, healthy cash generation with an advantage with its ESG product compliance and cost competitiveness, while the global macro is a tailwind – less competition from China combined with cheaper operations in Brazil.

To put some perspectives, Albemarle Corp – its main competitor, has already ran ~170% over the last year without explosive news and while having a less attractive financial profile – but being a much bigger diversified company.

The second tailwind for the industry is the global electrification happening around the world now while lithium is the most important component for batteries – which are globally getting cheaper and more efficient for households and businesses alike. If we look at Tesla’s success with Megapacks and the rebound for solar installations for households, on which I am overly bullish and is pushed by the Iran war, then demand for lithium should continue to increase, and if the commodity is also more expensive, profits for producers simply accelerates.

And both Albemarle and Sigma charts show this kind of anticipation by the market. As usual for the latter, the same chart patterns as always.

Now sitting below a strong resistance which creates the same condition than both IM and Firefly Aerospace: a breakout on volume triggers a buy on the retest as the trend is starting, while a rebound on the W50 triggers accumulation anticipating for a potential breakout.

If we start looking at valuation, the stock looks more expensive than its peers but it also has higher cash generation, healthier balance sheet, a premium for the potential revenue growth, its ESG compliance, accelerating demand for local supply chain and cost competitivity, with the risk being execution risk for its expansions.

Another name I would gladly buy on the right price action conditions.