Feb 4, 2026

Novo Nordisk disappointing Q4-25 results with a weak guidance despites strong prescriptions of GLP-1 pills

This will be a pretty rapid write up. The bull case was crystal clear: Novo Nordisk was a defensive/healthcare asset and those are in demand nowadays, they had clear growth lever with the new GLP-1 pill, at least a potential one. Low valuation, growth potential and defensive fundamentals. A combo I look at with a great smile nowadays.

It Started Well

And confirmations came from management as the GLP-1 pill did wonderful, one of the best pharma starts in terms of demand.

We knew it's going to be the best in terms of efficacy of 16.6% we had expected it to do well, but we did not think that after four weeks of introduction, we will have 170,000 people on the pill

It also, as expected, expanded the market as more than 80% of these newcomers were on their first GLP-1 treatment. The needle phobic thesis was true, and will remain true.

And It Got Bad

And yet… The only bear case I highlighted did materialize, big time; pricing won’t allow growth.

The pill is sold at ~$149 and even if most paid for it out of their pockets - which again highlights a massive demand for the product, it won’t be enough to move the needle (pun intended) for Novo compared to the $1,000+ injectables at their release.

Part of the volume demand comes from the lower price point. But it isn’t enough to bring Novo back to growth, at least not this year, and this was crystal clear with the company’s guidance.

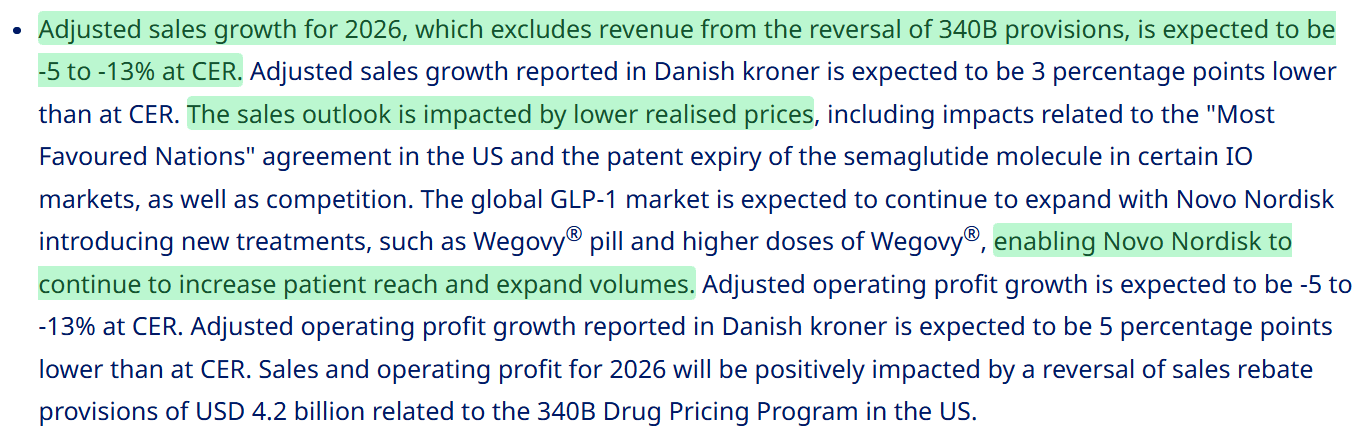

There are two key data in those few lines.

Novo expects a pretty sharp decline despite volume expansion. It certainly is hard to anticipate volume expansion for such a product, but a -5% revenue minimum doesn’t show optimism, far from it, despite a record launch...

Comparisons are made at comparable currency using 2024 rates. The dollar was strong then and as it plunged 8% since against the Danish krone, real decline will be much lower assuming no return to 2024 average for the dollar - with Trump’s comments I wouldn’t count on this happening.

It. Got. Bad.

Eli Lilly

On the contrary, the sun is shining on Eli Lilly which reported a massive quarter with 123% YoY growth for its injectable Zepbound and confirmed its pill coming H1-26, assuming FDA approval which they are working on. That said, to keep some hope, clinical trials are apparently better for Novo’s pill.

If you ask pretty much any patient, and certainly ask me, which one would you rather take? 17% weight loss or 12%? I know my answer, and we have seen the answer from 170,000 [patients] coming on very quickly.

Efficacy-wise, Novo's product, on the clinical trials at least, looks better. Tolerability looks quite attractive compared to [Lilly's orforglipron]. Novo actually might have an edge, and it will entirely depend on how they execute.

If those numbers are true, H2-26 or FY27 could be massive for Novo as they could take the lead back from Eli Lilly, and we’ve seen what a leader in obesity gets in the market - although pricing remains an issue even with a massive market as it’ll take Novo 10 patients to return as much as 1 patient for injectables early 2025.

But the potential combination of favorable comps and a growing market could do the trick end of 2026.

What Now?

There is nothing more to say about this quarter. The thesis was right to some extent; demand for the pill is massive, TAM will expand. but pricing won’t bring Novo back to growth and as I said in the thesis, without at least a 15% YoY quarterly growth, Novo doesn’t deserve anything near 6/7x sales, so with negative growth… There is no saying what Novo deserves.

I did open a small position a few days ago and I will be closing it. Being patient was once again the right move; we had no clear double bottom, no clear higher high & even with a bit of excitement the last weeks, the chart wasn’t that sexy.

My thesis is broken so I am out. That being said, I’ll keep Novo on my watchlist as the first half of 2026 is one thing but the prediction for their GLP-1 pill demand is almost impossible to get right, so that terrible guidance might be reviewed before H2-26, with maybe a better chart, more demand, a clear range… Valuation is very low at 4x sales but the market taught us again and again that cheap can get cheaper.

For now, it remains too early to go big on this name. Time might come and it’s 100% worth keeping it on our radar and following price action.

We have time. Patience is key.

——————————————————

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.